Build, protect, and grow your financial legacy with a plan that fits real life today.

Alfa Pride Financial helps families, entrepreneurs, and small business owners create practical wealth plans, retirement strategies, and protection for the people they love.

Financial planning, retirement, life insurance, long-term care

Also supporting entrepreneurs, small business owners, and healthcare clinics

Meet Alfa Pride Financial

Empowering your business, securing your future.

Supporting our community with service in the spirit of excellence.

Financial Planning & Wealth-Building

Retirement Strategy

Life Insurance & Long-Term Care

Medicare & Supplemental Health Plans

Business Funding & Employee Benefits

start here

Start With a Simple Financial Checkup

Many people believe their finances are on track, but hidden gaps in protection, liquidity, and retirement planning can create serious long-term risks.

Our Financial Risk & Protection Scorecard is a quick self-assessment that helps you identify potential vulnerabilities in your financial plan and see where improvements may be needed.

The process takes only a few minutes and provides a clear snapshot of your current financial position.

Identify hidden financial risks

Evaluate income protection and liquidity strength

Review retirement readiness and long-term planning

Receive a personalized financial wellness score

SERVICES

Your financial life, organized and supported in one place.

We help you move from scattered accounts and guesswork to a coordinated strategy that covers your income, family, health, and business interests.

For your household

Financial Coaching & Consulting

Start here

A clear, realistic plan to help you save, and protect what you are building, based on where you are right now and where you want to go.

Cashflow review and debt strategy

Savings and wealth accumulation planning

College, home, and legacy goals

Annuities

Guaranteed income

A strategy designed to help turn savings into reliable retirement income. Annuities can provide predictable payments, tax-deferred growth, and protection against the risk of outliving your money.

Lifetime income stream options

Fixed, indexed, and income annuity solutions

Tax-deferred growth and principal protection features

Life Insurance

Family protection

Protection for income, debts, and future goals so your family can stay rooted, even if life takes an unexpected turn.

Term, whole life, and universal life options

Coverage for income replacement and debt

Living benefits on eligible policies for serious illness

Long-Term Care Planning

Future care

A plan for care costs so your children and loved ones are not forced to carry the entire financial burden if you ever need extended care.

Standalone & hybrid long-term care options

Alternative & supplemental homecare plans

Cost-of-care estimates for your situation

Medicare Plans

Licensed guidance

Support reviewing Medicare options so you can make informed, confident choices about your health coverage in retirement.

Medicare Advantage (Part C) plan comparisons

Prescription Drug Plan (Part D) reviews

Medigap/Medicare Supplement plan education

Supplemental Health Plans

Extra protection

Supplemental coverage that pays cash benefits to you to help with out-of-pocket costs after an accident, serious diagnosis, or disability.

Accident insurance options

Cancer and critical illness coverage

Disability and related supplemental plans

For your business

Business Credit & Financing

Capital & credibility

Help separating your personal and business finances, building business credit, and exploring funding options through our lender network.

Business credit education and strategy

Lines of credit, term loans, and equipment financing

Multiple lenders and program types

Employee Retirement Plans

Workforce stability & long-term growth

Help employees build long-term financial security while strengthening retention and total compensation strategy.

SEP IRA and SIMPLE IRA options for small businesses

401(k) and qualified retirement plan coordination

Plan design guidance aligned with business size and budget

Education support to improve employee participation

Employee Benefits & HR Solutions

For employers

Access to benefits and HR solutions that can help you attract and retain staff without carrying the full burden alone.

Voluntary benefits and supplemental plans

PEO and HR solutions through vetted partners

Benefits education for staff

Who we serve

Serving families, entrepreneurs, and small businesses.

We work with people who are serious about getting organized, protecting what they have built, and creating a clearer path forward for themselves and the people who depend on them.

Households and families

First-time and experienced entrepreneurs

Small business owners and teams

Healthcare professionals and clinic leaders

Households and families

Families balancing rent or mortgage, childcare, debt, and support for parents or extended family members.

Parents planning for college, retirement, and legacy at the same time.

Single parents and blended households needing affordable protection.

Multigenerational homes where several people rely on one or two incomes.

Entrepreneurs & Small Business Owners

From side hustles to growing businesses, we help you protect your income, structure your entity, and think about funding and benefits the right way.

First-time founders forming LLCs and corporations.

Owners ready to separate business and personal finances.

Entrepreneurs seeking funding without predatory terms.

Healthcare Clinics & Professionals

Clinics and healthcare leaders managing staffing, benefits, and cashflow while still serving patients and communities.

Independent clinics facing margin and compliance pressure.

Leaders who want to improve benefits without breaking the budget.

Providers who also need personal planning and protection.

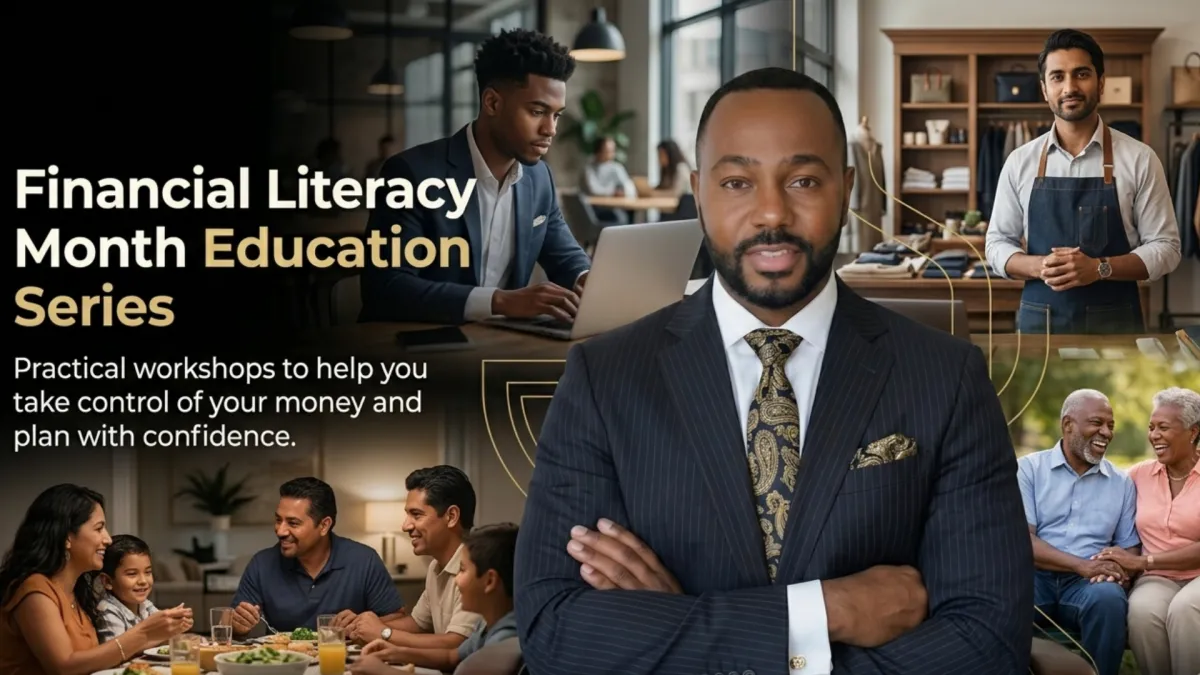

financial Workshops

Financial Literacy Education Series

This Financial Literacy Month series features six live educational webinars designed to help strengthen your financial foundation and make more informed decisions across every life stage.

What Participants Learn

Practical strategies for improving cash flow and managing expenses

How to reduce debt and avoid common financial pitfalls

Planning approaches for retirement beyond Social Security

Key principles of estate planning, including how to protect assets and provide for your family

Core financial concepts explained in clear, actionable terms

Financial Education That Empowers Better Decisions

Our interactive financial workshops provide practical education on key financial topics so participants can better understand their options and strengthen their long-term financial stability. Workshops are designed for community organizations, businesses, schools, and professional groups looking to provide valuable financial education in a clear, approachable format.

What Participants Learn

Practical strategies for building financial stability

How to identify and reduce common financial risks

Planning approaches for retirement, protection, and long-term goals

Key financial concepts explained in simple, actionable terms

Interactive planning tools

Start Here • Recommended

How Financially Protected Are You Right Now?

Use this quick scorecard to uncover hidden risks in your financial plan and see where you may be exposed.

Evaluate protection across income, savings, and liabilities

Identify gaps that could create financial setbacks

Understand how prepared you are for real-world risks

Get a clear starting point to strengthen your strategy

Takes less than 3 minutes

How Much Life Insurance Protection Does Your Household Actually Need?

Use this quick planning tool to estimate income replacement, debt coverage, and long-term obligations.

Identify existing financial commitments that need to be covered.

Estimate income replacement needs and align them with the appropriate coverage.

Determine how much is needed to settle your estate and avoid family burden.

Coordinate coverage with existing assets to maximize protection.

Will Your Retirement Income Be Enough?

Estimate your projected income and identify potential shortfalls.

Clarify your retirement vision, timeline, and lifestyle goals.

Estimate income needs and align them with Social Security, pensions, and savings.

Review investment, insurance, and long-term care options that match your comfort with risk.

Identify gaps and next steps you can start working on in the next 12 months.

Free resources

Client stories

What clients say about working with Alfa Pride Financial.

Real people, real situations, and a shared goal: save money, make money, and protect money for the long term.

About Alfa Pride Financial

Education first. Community-centered. Legacy-focused.

Alfa Pride Financial exists to help families and entrepreneurs eliminate financial vulnerabilities, safely grow assets, and protect what they are building, with a focus on practical, real-world challenges facing households and businesses.

Our mission is to help you save money, make money, and protect your money. It takes a certain level of skill to make money, but it takes a different level of skill to actually keep it.

Led by licensed financial professional Xavier Williams, Alfa Pride Financial combines financial planning, insurance, and business services into a practical roadmap that meets you where you are. We take time to understand your story, your responsibilities, and the people counting on you before making any recommendations.

We are not a one-size-fits-all agency. Every plan is tailored to your needs, built around education, and designed to support you for the long term, not just a single transaction.

Whether you are building a family, launching a business, caring for aging parents, or planning for retirement, our goal is simple: empower your business and secure your future with clear steps, not pressure.

Holistic view

Personal finances, protection, and business planning considered together.

Community focus

Prioritizing everyday families and business owners who want straightforward, education-first guidance.

Education first

You will always understand your options before you decide what is right for you.

Contact us

Ready to talk about your next step?

Whether you are planning for retirement, reviewing life insurance, exploring long-term care, or looking for business support, a short conversation can help bring clarity to your next move.

Choose the path that fits you best. You can book a consultation directly, call our office, or send a message through the form and we will follow up within one business day.

Email: [email protected]

Phone: 833-382-6313

Please do not send sensitive personal information such as Social Security numbers or full account numbers through this form or by email.

This is a

© 2026 Alfa Pride Financial. All rights reserved.

Address: 1500 Astor Avenue, 2nd Floor, Bronx, NY 10469

Phone: Email: [email protected]

Alfa Pride Financial is an independent financial services agency providing financial planning, insurance, Medicare guidance, and business services. Insurance and Medicare products are offered through licensed agents, and product availability, features, and eligibility may vary by state and carrier. Insurance and Medicare services are available in California, Connecticut, New York (resident state), and Florida.

All information on this website is for general educational purposes only and is not intended as individualized tax, legal, investment, or accounting advice. Life insurance and related products are not savings or investment accounts, and policy features, riders, and benefits vary by carrier and state. Individuals should consult a qualified tax professional, attorney, or advisor for guidance specific to their situation.

Medicare guidance is limited to the plans we offer. We do not offer every plan available in your area; for a complete view of options, please contact Medicare.gov or 1-800-MEDICARE. Business funding services are provided through a network of independent lenders, and all loan approvals, terms, and conditions are determined solely by those lenders. No specific outcomes, approvals, or interest rates are guaranteed.

Font