Yes, it’s great that you have employee benefits at your job. However, don’t get too comfortable and overly confident. The reality is they are not enough to provide financial security. There are several downsides to those benefits you may not be aware of. Unfortunately, you may not realize this until it’s time for you to actually use them. To learn what they are, and how to address them, keep reading.

Group Disability Insurance

Disability insurance protects your income in the event you are disabled and not able to work and earn a living. If an employer offers disability coverage, most likely it is a short-term disability that covers you for anywhere from 9 - 52 weeks. If you experience a disabling event that lasts longer than the benefit period, it could be financially disastrous, forcing you to exhaust your personal savings and other assets to survive.

The fact that you don’t own the disability policy also means you can’t take the policy with you if you switch jobs or experience a period of unemployment. The employer can also cancel the policy at any time and choose not to replace it with coverage from another insurer. Many group policies also require you to be totally disabled to receive benefits. Your disability not meeting that classification would leave you on your own.

There are also caps on the amount of income replacement the benefit would actually pay, and it would be taxed because the premium payments for the policy were made on a pre-tax basis. So for example, if you made $100,000 annually, that places you in the 24% tax bracket. After taxes, you would bring home $76,000. A Short-term disability policy typically replaces 60% of your pre-tax salary. However, that 60% benefit would be taxed at the 24% tax level, leaving you with only $45,600 which is 46% of your annual salary.

Would you be able to survive on only 46% of your monthly salary? This would be a serious financial risk to your quality of life. To address this coverage gap, a personally owned, long-term disability policy can help to alleviate this vulnerability. Working with a financial advisor or another licensed financial professional can help you weigh your options and determine an appropriate plan for you.

If getting a personal policy is cost-prohibitive, you should look to social security. Create a profile for yourself on their site and review what is your current social security disability benefit entitlement. Knowing that number can help you financially prepare for any long-term disability events that may come your way. However, do be warned that qualifying for social security disability benefits is difficult and not easily obtained.

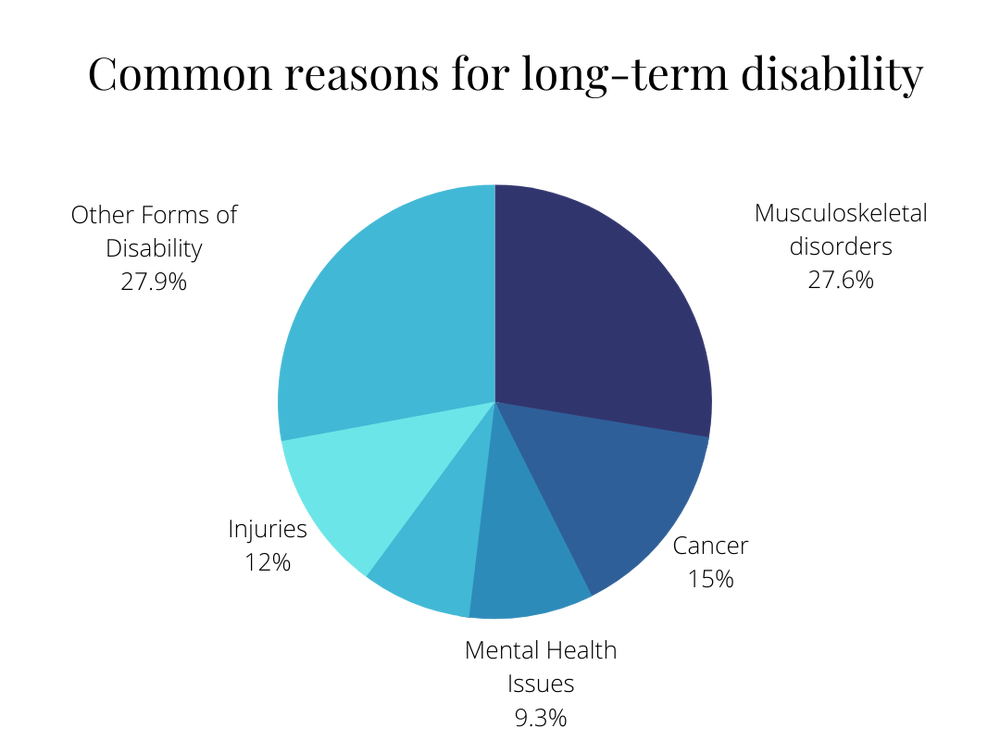

Please note that going without a plan to address a period of disability should not be taken lightly. According to the council disability awareness, one in four twenty-year-olds will experience a period of disability before they reach retirement age. Most disabilities are also not caused by accidents on the job. The highest causes are pregnancy, musculoskeletal disorders, cancer, injuries such as fractures, sprains, strains of muscles and ligaments, mental health issues, and circulatory issues such as heart attacks and strokes.

Group Life Insurance

Life insurance helps to replace your income for your family if you pass away too soon when they are financially dependent on you. It comes with a large host of other living benefits that you can take advantage of, which will be discussed in future posts.

Like group disability policies, group life insurance is not portable, so you can’t take it with you if you decide to change jobs. Since most employers only provide term life insurance, if you do decide to leave, you will be forced to convert your policy to a permanent type of product which would make your premium payments skyrocket. If you are unable to afford the premium payments you would most likely have to relinquish the policy and leave your family financially vulnerable.

Group policies also come with coverage caps which are determined by the employer. Some may limit the amount of insurance you can get to just $250,000, even though you may need $1,000,000 or more in coverage to replace your income for your family and satisfy other financial commitments. Healthier individuals also pay the same premiums as those who are less healthy and have a higher risk within the group policy. These healthy employees are being overcharged, and the less healthy ones are getting considerable savings on their coverage.

To address this issue, group life insurance should not be the only type of policy you have in place. It should be supplemented with a stand-alone policy that you are paying for outside of your employer. You will get more favorable rates and a policy customized to your unique financial situation.

Qualified Retirement Plans

A qualified retirement plan is a retirement plan that meets certain IRS requirements and grants them Certain tax benefits. Examples of qualified plans are pensions, 401(K’s), 403(B’s)/Tax Sheltered Annuities, and IRA’s. Plans such as 401 (K’s), 403 (B’s), and IRA’s help you save for retirement while lowering your taxable income but pensions are totally funded by your employer.

Your contributions in 401(K) and 403(B) plans are directly invested in the stock market and you have no control over when trades are made. So whether investments are priced high or low your account is processing buys which can impact your growth. You may also have limitations on how often you can make adjustments to your plan to ensure your portfolio is in line with your risk tolerance.

401(K) and 403(B) plans are heavily regulated by the federal government which is great, however, the administration of the plans comes with high fees that are passed on to you. These plans offer limited mutual fund options which come with their own expenses. These fees eat into your growth and can cost you tens to hundreds of thousands of dollars if you’re invested for a long period of time, and have a high account balance.

When it is time to start taking distributions from these plans in retirement, you can end up paying a lot more in taxes. If you were great at saving, you will definitely be in the same tax bracket as when you were working or may even be in a higher one. At that point, you will owe taxes on all the contributions you made while working because they were invested in the plan on a pre-tax basis. All the growth in the account will also be subjected to capital gains taxes, increasing your tax liability.

To address this tax risk, you should contribute enough to your employer-sponsored plan to receive the company match. Anything excess of that amount that you want to contribute to retirement savings can be placed into tax-free sources of income such as a Roth IRA or permanent life insurance product that has been properly structured to maximize the growth of the cash value. This approach will allow you to diversify your savings, spread out, and lower your tax liability, so you can enjoy a comfortable, worry-free retirement.

Employee group benefits are great to have, but they are not the end-all-be-all solutions to securing your financial future. They are just a starting point. Awareness of their shortcomings will allow you to properly prepare for all of your expected and unexpected life events.

There is no better time to re-evaluate your current situation than the present. Connect with a licensed financial professional at Alfa Pride Financial, to assess where you are on your financial journey, and get the financial keys to a worry-free life.

Comments ()